Article

Introduction to the Commercial Seed Market

The global commercial seed market is undergoing robust expansion, driven by growing global food demand, advancements in seed technologies, and the increasing adoption of high-yielding and pest-resistant crop varieties. According to Cognitive Market Research, the market size for commercial seeds is projected to reach USD 86,821.8 million in 2024 and is expected to grow significantly to USD 170,474.7 million by 2032, registering a strong CAGR of 8.80%. This growth is supported by increasing investments in agricultural innovation, precision farming practices, and supportive government policies aimed at improving crop productivity and food security. Commercial seeds are specifically cultivated and processed for use by farmers, offering advantages such as higher yield potential, better resistance to pests and diseases, improved tolerance to climatic stresses, and consistent quality. The rising global population, combined with decreasing arable land per capita, is putting pressure on farmers to produce more with less. In response, demand for genetically modified (GM) and hybrid seeds has surged, particularly for crops such as corn, soybean, cotton, and canola. Additionally, the rising popularity of organic and specialty crops in developed markets is also creating opportunities for specialty commercial seed providers.

Top Companies Operating in the Commercial Seed Industry Worldwide

- Bayer Group

- Corteva

- Syngenta Global AG

- KWS SAAT SE & Co. KGaA

- Vilmorin-Mikado

- Rijk Zwaan Zaadteelt en Zaadhandel B.V.

- Sakata Seed America

- Takii & Co., Ltd.

- Advanta Seeds

- Dow

Criteria for Comparing Companies in the Commercial Seed Market

According to Cognitive Market Research, companies competing in the commercial seed market are often compared based on factors such as seed performance (yield, resistance, adaptability), research and development capabilities, product portfolio diversity, and geographic presence. Companies that offer seeds suited to a wide range of agro-climatic conditions and that back their products with strong agronomic support tend to gain a competitive edge. Furthermore, the ability to deliver consistent seed quality through advanced breeding technologies such as CRISPR gene editing, marker-assisted selection, and transgenic traits has become a key differentiator in this industry. Another important aspect is the extent to which companies provide value-added services such as customized seed recommendations, digital farming platforms, and sustainability-driven crop solutions. Major players such as Bayer CropScience, Corteva Agriscience, Syngenta Group, and BASF are investing heavily in developing next-generation seeds that cater to both conventional and organic farming systems. Their strategies include expanding into emerging economies, partnering with local agribusinesses, and aligning their offerings with climate-smart agriculture initiatives. As climate change poses increasing challenges to global food production, the role of resilient, high-performing commercial seeds will become even more vital. Companies that combine advanced breeding techniques with farmer-centric solutions, sustainability goals, and regional customization will continue to lead in this evolving and increasingly essential market.

Top Manufacturing Companies of Commercial Seed:

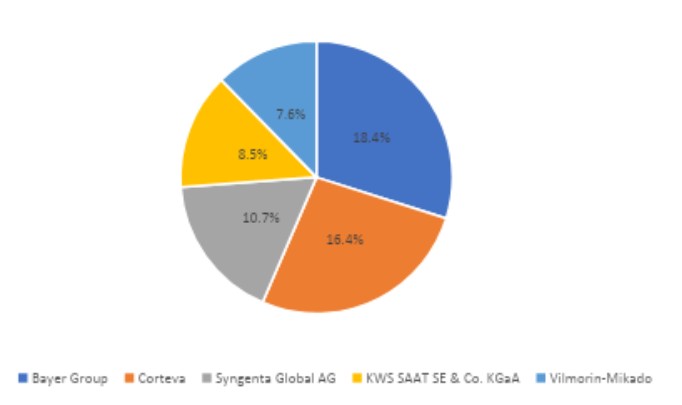

Bayer Group, Corteva, Syngenta Global AG, KWS SAAT SE & Co. KGaA, and Vilmorin-Mikado are the key players in the Commercial Seed Market

Bayer Group

Bayer Group leads the Commercial Seed Market with a substantial 18.4% market share, driven by its wide-ranging portfolio of high-yielding, disease-resistant seeds and its long-standing commitment to agricultural innovation. The company, through its Crop Science division (which includes the legacy of Monsanto), delivers cutting-edge seed technologies across corn, soybean, cotton, canola, and vegetable seeds. Bayer’s strong R&D infrastructure, coupled with advances in biotechnology and trait development, has positioned it as a global leader capable of meeting diverse farming needs under varying climatic and agronomic conditions.

Corteva

Corteva holds a prominent 16.4% share in the Commercial Seed Market, reflecting its strength as a dedicated agriculture-focused company formed through the merger of Dow AgroSciences and DuPont Pioneer. The company’s success stems from its comprehensive seed offerings in corn, soybean, sunflower, rice, and other crops, which are widely used by commercial growers across the globe.

Syngenta Global AG

Syngenta Global AG commands a solid 10.7% market share in the Commercial Seed Market, primarily due to its robust seed development in corn, soybean, cereals, rice, and vegetable crops. Backed by Chinese state-owned ChemChina, Syngenta has been expanding its global seed footprint through aggressive investments in trait development, hybrid research, and seed technology platforms.

KWS SAAT SE & Co. KGaA

KWS SAAT SE & Co. KGaA holds an 8.5% share in the global Commercial Seed Market, known for its excellence in sugar beet, corn, cereals, and oilseed rape seeds. Headquartered in Germany, KWS has established itself as a leader in seed breeding, with a legacy of over 165 years in developing high-performance cultivars suited for different agro-climatic zones.

Vilmorin-Mikado

Vilmorin-Mikado, part of the Limagrain Group, captures 7.6% of the Commercial Seed Market, specializing in vegetable and field crop seeds. With a rich breeding heritage and a diverse portfolio covering over 80 vegetable species, Vilmorin-Mikado supports global food security through its commitment to genetic innovation and plant health.

Potential Threats to Top Five Players in the Commercial Seed Market

CMR found that emerging companies in the commercial seed market namely Rijk Zwaan Zaadteelt en Zaadhandel B.V., Sakata Seed America, Takii & Co., Ltd., Advanta Seeds, and Dow are well-positioned to pose considerable threats to long-standing industry leaders. These firms are leveraging a combination of focused innovation, regional strength, and strategic global expansion to challenge the dominance of the top five players. Headquartered in the Netherlands, Rijk Zwaan Zaadteelt en Zaadhandel B.V. has built a reputation for high-quality vegetable seeds backed by robust R&D investments. Their strategy revolves around close collaboration with growers and food supply chains, enabling the development of customer-centric seed varieties. With a strong presence in over 100 countries, Rijk Zwaan’s emphasis on resistance breeding and climate-resilient crops positions it as a serious competitor in the global seed space. Sakata Seed America, a subsidiary of Japan’s Sakata Seed Corporation, focuses extensively on vegetable and ornamental seeds. The company’s strength lies in its investment in biotechnology and disease resistance, alongside its well-established distribution network in the Americas. This regional dominance, coupled with its commitment to innovation, enables Sakata to encroach on market segments traditionally held by larger seed corporations.

Takii & Co., Ltd., another Japan-based player, stands out for its heritage in seed development and pioneering work in hybrid seeds. Takii’s investments in seed genetics and variety improvement, particularly for vegetable crops, give it a technological edge. Its global breeding centers and collaborations with research institutions enhance its capability to deliver locally adapted seed solutions undermining the foothold of top-tier companies in diverse agro-climatic zones. Advanta Seeds, part of the UPL group, brings a strong portfolio of field and vegetable seeds, especially in emerging economies. The company's focus on hybrid and high-yielding varieties tailored to regional agricultural needs has spurred its rapid growth in Asia, Africa, and Latin America. Advanta’s competitive pricing, coupled with its farmer-centric approach, enables it to build brand loyalty and eat into the market share of incumbents. Dow, though historically known for its broader agricultural and chemical portfolio, has strategically positioned its seed division to take on major players. Its integrated R&D capabilities and access to proprietary biotechnologies allow Dow to deliver genetically advanced seed varieties across row crops. This innovation pipeline, alongside synergies from its agrochemical business, enhances its value proposition to farmers, putting pressure on established leaders. These emerging players are reshaping the commercial seed landscape through innovation, strategic alliances, and deep regional insights. Their ability to adapt to evolving agronomic needs and regulatory shifts makes them formidable competitors, capable of disrupting the dominance of long-standing global seed giants.

Conclusion

Advancing Food Security Through Sustainable Innovation and Smart Agricultural Practices

The commercial seed market is on a robust growth trajectory, expected to expand from USD 86,821.8 million in 2024 to USD 170,474.7 million by 2032, growing at a CAGR of 8.80%. This growth is being driven by global demand for increased agricultural productivity, changing dietary trends, and the pressing need for climate-resilient farming solutions. Leading players such as Bayer CropScience, Corteva Agriscience, Syngenta Group, BASF SE, and KWS SAAT SE continue to dominate through their proprietary technologies, global supply chains, and strong farmer networks. However, emerging challengers such as Rijk Zwaan, Sakata Seed America, Takii, Advanta Seeds, and Dow are actively redefining competitive dynamics. Their agility, innovation, and region-specific strategies are helping them break into markets that were previously the stronghold of global conglomerates. For new entrants and mid-sized players, the road to success involves embracing sustainability, investing in next-generation traits, and building digital and agronomic service ecosystems that empower farmers. Market dynamics are increasingly favoring companies that can deliver high-performing, adaptable, and environmentally responsible seeds. As the global population grows and climate change accelerates, the commercial seed market will play a vital role in shaping the future of food security. The collaboration between governments, research bodies, legacy players, and disruptive entrants will be critical to ensure that agriculture remains productive, inclusive, and sustainable in the years ahead.

Article Details

-

Author Pratik Shirsath

-

Published 07 Jun 2025

-

Last Updated 13 Jun 2025

-

Reading Time~3 minutes

Related Reports

Get a Custom Report

Interested in a similar analysis for your market? Our experts can deliver a customized report.

Contact Our ExpertsMore Articles

Explore all published articles across 30+ industry verticals.

View All Articles