Article

Introduction to the Stainless Steel Market

The Stainless Steel market is witnessing steady expansion, driven by increasing demand across industries such as construction, automotive, aerospace, and consumer goods. According to Cognitive Market Research, the market is valued at USD 185,624.8 million in 2024 and is projected to reach USD 318,938.0 million by 2032, growing at a CAGR of 7.00%. Stainless steel's durability, corrosion resistance, and aesthetic appeal make it a preferred material for applications ranging from industrial machinery and infrastructure to household appliances and medical instruments. The rapid urbanization and industrialization in emerging economies are fueling the need for high-performance materials, particularly in construction and transportation sectors. Additionally, growing environmental concerns and government regulations promoting the use of recyclable materials have strengthened the demand for stainless steel, given its high recyclability and long lifecycle. Technological advancements in steel manufacturing, including electric arc furnaces and vacuum degassing processes, have significantly improved the quality and efficiency of stainless steel production. The market is also benefiting from innovations in alloy compositions that enhance strength, flexibility, and resistance to extreme conditions, expanding stainless steel's applicability in advanced engineering solutions. The shift toward sustainable infrastructure and the increasing adoption of stainless steel in renewable energy projects, such as solar panel mounting structures and wind turbine components, are further accelerating market growth. The Asia-Pacific region, led by China, India, and Japan, remains the dominant market, supported by strong industrial output, expanding construction activities, and rising investments in smart cities. Meanwhile, North America and Europe continue to drive demand through high-end applications in automotive, healthcare, and aerospace sectors.

Criteria for Comparing Companies in the Stainless Steel Market

Cognitive Market Research assesses companies in the Stainless Steel market based on parameters such as production capacity, product innovation, geographical reach, sustainability initiatives, and financial performance. Revenue and market share are key indicators of a company’s dominance, reflecting its ability to meet large-scale industrial demand and maintain strong customer relationships. Companies with extensive production capabilities and diverse product offerings, including austenitic, ferritic, martensitic, and duplex stainless steel grades, hold a competitive advantage by catering to various end-user industries.

Innovation in stainless steel production processes is a significant differentiator in the market. Companies that invest in advanced metallurgical technologies, automation, and energy-efficient manufacturing methods can enhance product quality and reduce production costs. Sustainability has become a crucial factor in market competitiveness, with leading players focusing on reducing carbon footprints through scrap-based recycling, energy-efficient production techniques, and eco-friendly alloy compositions. The ability to produce high-performance stainless steel with enhanced mechanical properties, improved corrosion resistance, and lightweight characteristics is essential for serving high-growth industries such as aerospace, medical devices, and electric vehicles.

Geographical presence is another important factor in assessing market position. Companies with a strong foothold in rapidly industrializing regions such as Asia-Pacific can leverage growth opportunities in construction, transportation, and heavy machinery sectors. Meanwhile, North American and European firms are focusing on value-added stainless steel products, targeting specialized applications in medical technology, food processing, and precision engineering. A well-established supply chain and distribution network, including partnerships with raw material suppliers and end-user industries, further strengthen a company’s market standing. Strategic collaborations, mergers, and acquisitions play a pivotal role in market leadership. Companies that expand their global footprint through joint ventures and investments in production facilities across key regions can capitalize on increasing demand. Leading market players such as Outokumpu, Acerinox, POSCO, Nippon Steel, and ArcelorMittal are leveraging technological advancements, product diversification, and sustainability initiatives to enhance their competitive edge. As industries increasingly prioritize durable and environmentally friendly materials, companies that emphasize innovation, efficiency, and strategic expansion will maintain a stronghold in the evolving Stainless Steel market.

Top Companies Operating in the Stainless Steel Industry Worldwide

- ArcelorMittal S.A.

- POSCO

- Baosteel Group Corporation

- Acerinox S.A.

- Jindal Stainless Group

- Aperam S.A.

- Nippon Steel Corporation

- Outokumpu Oyj

- Acciai Speciali Terni S.p.A.

- Yieh Corporation

Top Manufacturing Companies of Stainless Steel:

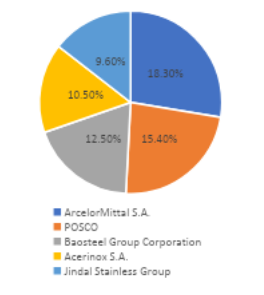

ArcelorMittal S.A., POSCO, Baosteel Group Corporation, Acerinox S.A., and Jindal Stainless Group are the key players in the Stainless Steel Market

ArcelorMittal S.A.

ArcelorMittal S.A. leads the Stainless Steel Market with an 18.30% market share, solidifying its position as the largest global producer of steel and stainless steel solutions. The company offers a comprehensive range of stainless steel products, including flat-rolled, long, and tubular stainless steel, catering to industries such as construction, automotive, energy, and consumer goods. ArcelorMittal’s state-of-the-art production facilities, advanced metallurgical expertise, and commitment to sustainability have made it a dominant force in the sector.

POSCO

POSCO holds a 15.40% market share, recognized as one of the world’s leading stainless steel producers, particularly in the Asia-Pacific region. The South Korean steel giant specializes in high-performance stainless steel grades for applications in shipbuilding, medical devices, food processing, and infrastructure development. POSCO's premium stainless steel products, including austenitic, ferritic, and duplex stainless steel, are renowned for their strength, corrosion resistance, and superior surface finishes.

Baosteel Group Corporation

Baosteel Group Corporation commands a 12.50% market share, making it one of China’s largest stainless steel producers with a growing international presence. The company manufactures a diverse range of high-strength and precision-engineered stainless steel products, catering to industries such as transportation, aerospace, heavy machinery, and household appliances. Baosteel's focus on high-grade, corrosion-resistant stainless steel has positioned it as a key supplier to China’s industrial and infrastructure sectors.

Acerinox S.A.

Acerinox S.A. holds a 10.50% market share, recognized as a leading European stainless steel manufacturer with a strong international footprint. The company specializes in flat-rolled and long stainless steel products, serving sectors such as architecture, renewable energy, food processing, and industrial equipment. Acerinox is known for its high-quality stainless steel grades, advanced surface finishes, and corrosion-resistant alloys, making it a preferred choice for critical infrastructure projects and specialized industrial applications.

Jindal Stainless Group

Jindal Stainless Group holds a 9.60% market share, making it India’s largest stainless steel manufacturer and a key global player in the market. The company produces a wide range of stainless steel solutions, including coils, sheets, plates, and precision strips, catering to industries such as transportation, construction, healthcare, and consumer goods. Jindal Stainless is known for its cost-effective yet high-performance stainless steel products, making it a preferred supplier for domestic and international markets.

Potential Threats to Top Five Players in the Stainless Steel Market

CMR found that the stainless steel market is a dynamic industry driven by demand from sectors such as construction, automotive, aerospace, and consumer goods. Established leaders like Acerinox S.A., POSCO, Baosteel Group, Jindal Stainless, and ThyssenKrupp Stainless have maintained dominance through extensive production capacities, advanced manufacturing technologies, and strong global distribution networks. However, emerging players, including Aperam S.A., Nippon Steel Corporation, Outokumpu Oyj, Acciai Speciali Terni S.p.A., and Yieh Corporation, are reshaping the competitive landscape by leveraging innovations, cost efficiency, and strategic market expansion.

One of the major threats to the top five players comes from fluctuating raw material prices, particularly nickel and chromium, which directly impact production costs. Emerging manufacturers, often backed by government incentives or located in regions with cost-effective resource procurement, pose a significant challenge to established firms. Additionally, sustainability concerns are pushing the industry toward greener production methods. Companies investing in carbon-neutral processes and recycling technologies are gaining an advantage, making it imperative for traditional players to accelerate their sustainability efforts to maintain competitiveness.

Conclusion

Investments in Sustainable Manufacturing, High-Performance Alloys, and Digitalization Are Essential for Long-Term Success in the Stainless Steel Market

The stainless steel industry is undergoing a significant transformation driven by environmental regulations, increasing demand for advanced materials, and the rapid adoption of digital technologies across manufacturing and supply chain operations. As industries such as construction, automotive, aerospace, and medical devices increasingly prioritize sustainability and efficiency, the demand for stainless steel products that meet these evolving requirements continues to rise. To remain competitive in this shifting landscape, both established and emerging players must focus on sustainable production practices, material innovation, and operational efficiency. Investing in energy-efficient manufacturing processes, such as electric arc furnaces (EAFs) and hydrogen-based steelmaking, can help companies significantly reduce their carbon footprint while enhancing cost efficiency. Additionally, the development of high-performance stainless steel alloys tailored for specialized applications such as lightweight, corrosion-resistant grades for electric vehicles or heat-resistant variants for industrial machinery can offer manufacturers a competitive edge. Companies that proactively engage in research and development to create advanced, high-strength alloys will be well-positioned to meet the increasing demand for durable and sustainable stainless steel solutions.

Beyond material and process innovations, the integration of digital technologies is becoming a defining factor for long-term success in the industry. Smart manufacturing techniques, including AI-driven predictive maintenance, automation, and blockchain-based supply chain tracking, can improve production efficiency, reduce operational costs, and enhance transparency across global supply networks. Companies that leverage digitalization to streamline inventory management, monitor real-time production data, and optimize resource utilization will gain a significant advantage in maintaining supply chain resilience and meeting customer expectations. Furthermore, strategic collaborations with end-user industries will play a crucial role in driving market expansion. Partnerships with infrastructure developers, renewable energy firms, and electric vehicle manufacturers can open new revenue streams and foster long-term growth opportunities. Targeting emerging markets, particularly in regions experiencing rapid industrialization and urban development, can also help stainless steel manufacturers establish a strong foothold in high-growth areas. By adopting these forward-thinking strategies, new entrants can successfully carve out a niche in the stainless steel market while competing effectively with industry leaders. Ultimately, companies that commit to sustainable innovation, digital transformation, and strategic market expansion will be best positioned to thrive in the evolving stainless steel industry. As global industries shift towards environmentally friendly solutions and more advanced material applications, the manufacturers that align their operations with these trends will not only ensure long-term success but also contribute to a more sustainable and efficient future for stainless steel production.

Article Details

-

Author Sneha Mali

-

Published 04 Apr 2025

-

Last Updated 16 Jun 2025

-

Reading Time~3 minutes

Related Reports

Get a Custom Report

Interested in a similar analysis for your market? Our experts can deliver a customized report.

Contact Our ExpertsMore Articles

Explore all published articles across 30+ industry verticals.

View All Articles