Article

Introduction to the Inverter Market

The global Inverter market is experiencing dynamic growth, underpinned by the rapid expansion of renewable energy systems, increasing energy storage solutions, and the rising need for efficient power backup technologies. According to Cognitive Market Research, the market is valued at USD 17,524.8 million in 2024 and is projected to reach USD 59,464.9 million by 2032, expanding at an impressive CAGR of 16.50%. Inverters play a critical role in converting direct current (DC) into alternating current (AC), making them essential components in solar photovoltaic systems, uninterruptible power supplies (UPS), electric vehicles (EVs), and various industrial and residential applications. This surge in demand is driven by increasing investments in solar power infrastructure, growing reliance on electric mobility, and the rising need for dependable and energy-efficient solutions in both developed and developing regions.

The global shift toward clean energy and decarbonization is creating a robust demand for solar inverters, which form the backbone of grid-tied and off-grid renewable energy systems. Additionally, the adoption of energy storage systems across residential, commercial, and utility-scale applications is propelling the demand for hybrid and battery-based inverters. In the electric vehicle space, inverters are critical for motor control and energy efficiency, supporting the ongoing transition toward electrified transportation. Government incentives, favorable policies promoting solar and EV adoption, and the declining cost of photovoltaic modules are further accelerating inverter deployment. Markets in Asia-Pacific, particularly China, India, and Southeast Asia, are leading the charge, while North America and Europe continue to grow through technological innovation and policy-driven infrastructure upgrades.

Top Companies Operating in the Inverter Industry Worldwide

- Huawei Technologies Co. Ltd.

- Power Electronics S.L.

- SUNGROW

- SMA Solar Technology AG

- Fimer Group

- Delta Electronics Inc.

- ABB Ltd.

- TMEIC (Toshiba Mitsubishi-Electric Industrial Systems Corporation)

- Schneider Electric

- Ginlong Technologies (Solis)

Criteria for Comparing Companies in the Inverter Market

Cognitive Market Research evaluates inverter market participants based on key performance indicators such as product portfolio diversity, innovation capacity, energy efficiency standards, scalability, and regional footprint. Companies with a broad range of inverter products covering string inverters, central inverters, microinverters, hybrid inverters, and EV inverters are better positioned to meet the varied demands of different end-user segments including residential, commercial, and utility-scale installations. Technological advancements, such as smart inverters with remote monitoring capabilities, grid-forming functions, and AI-based diagnostics, serve as differentiators in a highly competitive market. Efficiency and compliance with international energy standards (like UL, IEC, and BIS) are central to product competitiveness. Companies investing in R&D to increase inverter conversion efficiency, reduce harmonic distortion, and enhance thermal performance are attracting a broader customer base. Moreover, manufacturers that provide modular and scalable inverter solutions can accommodate the evolving energy needs of consumers and grid operators alike. Integration of IoT, real-time analytics, and adaptive control systems into inverter platforms is becoming increasingly important for grid stabilization and performance optimization, particularly in distributed energy networks. A global presence and a strong after-sales service infrastructure are crucial for building trust and retaining customers in both emerging and mature markets. Companies that establish local manufacturing units or service centers in fast-growing regions such as Southeast Asia, Latin America, and the Middle East gain a strategic edge in meeting regulatory requirements and reducing delivery timelines. Strategic partnerships with solar developers, battery storage firms, and EV manufacturers further bolster market influence and supply chain resilience.

Prominent players such as Huawei, Sungrow, and SMA Solar Technology are driving innovation in the inverter market through advanced engineering, enhanced grid connectivity features, and sustainability-oriented designs. Their focus on digital transformation, cost-effectiveness, and high-performance inverter systems positions them at the forefront of the industry. As the global energy landscape continues to evolve, the companies that combine technological excellence with strategic adaptability are poised to lead the next wave of growth in the inverter market.

Top Manufacturing Companies of Inverter:

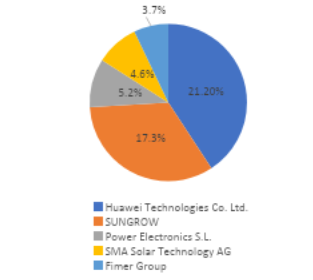

Huawei Technologies Co. Ltd., SUNGROW, Power Electronics S.L., SMA Solar Technology AG, and Fimer Group, are the key players in the Inverted Market

Huawei Technologies Co. Ltd.

Huawei Technologies Co. Ltd. leads the global Inverter Market with a dominant 21.20% market share, driven by its robust portfolio of smart solar inverters and deep integration of AI and IoT technologies. The company’s offerings include residential, commercial, and utility-scale solar inverters, which are recognized for their high efficiency, reliability, and intelligent monitoring capabilities. In 2023, Huawei reported significant revenues from its digital power segment, which includes solar inverters, reflecting strong global demand for energy-efficient and connected solar solutions.

SUNGROW

SUNGROW follows with a substantial 17.3% market share, solidifying its status as one of the most prominent inverter suppliers globally. The company offers a broad range of PV inverter solutions, including string, central, and hybrid inverters, which are known for their robust design, grid support capabilities, and efficiency levels exceeding 98%. In 2023, SUNGROW saw a surge in international installations, especially in Europe, Southeast Asia, and the Americas, which contributed to its growing revenue base.

Power Electronics S.L.

Power Electronics S.L. holds a 5.2% market share, establishing itself as a specialist in utility-scale solar and energy storage inverters, especially in markets like Spain, the U.S., and Latin America. The company focuses on central inverters for large-scale solar farms and grid support solutions, providing robust systems that are built to operate under extreme environmental conditions. In 2023, Power Electronics expanded its global footprint with strategic contracts for renewable energy projects in South America and North Africa.

SMA Solar Technology AG

SMA Solar Technology AG commands a 4.6% share of the global inverter market and is widely recognized for its German-engineered quality and innovation in inverter technologies. The company offers a full range of string, hybrid, and system-integrated inverters suitable for residential rooftops, commercial installations, and utility-scale solar farms. In 2023, SMA experienced a resurgence in European markets, especially in Germany, Italy, and the Netherlands, driven by policy support for renewable energy and energy independence.

Fimer Group

Fimer Group holds a 3.7% market share and has established a strong presence in the residential and commercial solar inverter segment, especially after acquiring ABB’s solar inverter business in 2020. The company offers a variety of string, central, and hybrid inverters, known for their compact design, ease of installation, and compatibility with energy storage systems. In 2023, Fimer expanded its sales channels across Europe, India, and parts of Africa, reflecting its commitment to serving both mature and emerging solar markets.

Potential Threats to Top Five Players in the Inverter Market

The global inverter market is witnessing intensified competition as emerging players steadily narrow the gap with leading incumbents like Delta Electronics Inc., ABB Ltd., TMEIC, Schneider Electric, and Ginlong Technologies (Solis). These top companies maintain a stronghold through their well-established distribution networks, comprehensive product portfolios, and significant R&D capabilities. However, the market landscape is rapidly evolving due to increasing demand for renewable energy integration, advanced energy storage systems, and intelligent power management solutions. New entrants are capitalizing on these trends to disrupt traditional dynamics. Their strategic moves ranging from launching high-efficiency solar inverters and hybrid systems to adopting digital monitoring platforms are enabling them to penetrate both mature and emerging markets with increasing ease. Players such as Ginlong Technologies (Solis) have gained notable traction through cost-effective residential and commercial solar inverters, especially in high-growth markets such as India and Southeast Asia. Meanwhile, Schneider Electric’s dominance is being tested by companies offering specialized solutions for microgrid and off-grid applications, areas where tailored and flexible inverter systems are in demand. TMEIC, traditionally strong in industrial applications, is now encountering rising competition from agile players that focus on modular inverter designs and IoT integration for predictive maintenance. ABB Ltd., with its broad global footprint, is increasingly challenged by companies leveraging region-specific strategies and local manufacturing to undercut prices while meeting performance standards. Delta Electronics Inc., while a leader in power conversion solutions, is witnessing heightened rivalry from firms introducing AI-powered inverters capable of dynamic load balancing and grid synchronization. These developments underscore a shifting competitive landscape where innovation and adaptability outweigh size alone.

Conclusion

Investments in digitalization, energy efficiency, and regional expansion are vital for achieving long-term competitiveness in the Inverter Market

The inverter market is poised for accelerated growth, driven by surging demand for renewable energy systems, electric vehicles, and smart grids. From residential solar rooftops to industrial automation and utility-scale applications, inverters play a critical role in optimizing energy usage and maintaining power quality. Leading players like ABB Ltd., Delta Electronics Inc., and Schneider Electric have long held a strong presence through their technological capabilities and expansive distribution systems. However, the emergence of agile and tech-savvy competitors is reshaping market dynamics. These new entrants are bringing fresh perspectives and specialized solutions to address evolving customer expectations highlighting that market leadership today hinges as much on innovation and adaptability as it does on legacy scale. To remain competitive in this dynamic environment, companies must invest in digital transformation, R&D, and customer-centric solutions. Developing AI-powered, IoT-enabled, and energy storage-compatible inverters will be essential to meeting next-generation energy demands. Additionally, embracing sustainable practices such as using recyclable components, enhancing inverter lifespan, and improving energy conversion efficiencies will align businesses with global environmental goals while reducing operational costs over time. Market expansion strategies, particularly in underpenetrated regions with growing renewable adoption, must be supported by robust local partnerships and tailored product offerings that reflect regional energy needs and regulatory frameworks. In the coming years, the ability to offer integrated, smart, and sustainable energy solutions will define market leaders in the inverter industry. Companies that adapt quickly, prioritize innovation, and remain attuned to customer and regulatory demands will be best positioned to drive lasting success in this high-growth market.

Article Details

-

Author Kalyani Raje

-

Published 19 May 2025

-

Last Updated 16 Jun 2025

-

Reading Time~3 minutes

Related Reports

Get a Custom Report

Interested in a similar analysis for your market? Our experts can deliver a customized report.

Contact Our ExpertsMore Articles

Explore all published articles across 30+ industry verticals.

View All Articles